Between Inflation and Recession

What can Greek mythology teach us about how the Fed works?

[Note: as we’re establishing this Substack, we have made all posts free to subscribers. We’re working toward offering a second post in some weeks focusing on real-world observations which will be available only to paid subscribers. This is a free sample of that type of post.]

Where are We Now with Inflation?

If you’re like most people, you probably don’t anxiously await the monthly release of inflation data by the U.S. Bureau of Labor Statistics.

But, what’s your guess as to the most recently released year-over-year U.S. inflation rate (as of September 2024)?

Is it above average, average, or below average historically? Read on and we’ll answer the question below.

But first, let’s use a bit of Greek mythology to set up this post.

Between Scylla and Charybdis

In Homer’s epic poem, The Odyssey, Odysseus, king of Ithaca, faces many perils as he tries to return home to his beloved wife Penelope in the aftermath of the Trojan War. Among the many challenges our hero faces is navigating the Strait of Messina, guarded on one side by the six-headed sea monster Scylla and on the other by the giant whirlpool Charybdis.

Less dramatic, but more relevant today, is the ongoing challenge the Federal Reserve faces in trying to navigate the way between Inflation and Recession.

The Feds instrument of choice in facing this challenge is their ability to set short-term interest rates.

In the midst of the 2008 recession, triggered by a global financial crisis, the Fed lowered rates to nearly zero. The goal of lower interest rates was to make it easier for people and businesses to borrow and spend money, with the hope that it would jump-start the economy.

Interest rates stayed historically low for an extended period of time as the economy slowly recovered.

Fast forward to early 2020, interest rates had remained below average for over a decade. Then the pandemic hit.

Throughout lockdown, people stayed home and their wallets stayed with them.

Eventually, the pandemic subsided and people got back to work and got back to spending money.

But there was a problem. During the pandemic, companies curtailed their production of many products. There was no quick fix for these supply shortages and prices surged, not just in the US, but across the globe.

Central banks were now faced with a different problem. They needed people to spend less money until supply and demand regained some semblance of balance.

In an effort to address rising prices, the Fed began raising interest rates during the summer of 2022 and continued to do so for two years, constantly monitoring the effects of their actions.

This process of using interest rates to affect spending is hardly an exact process and their concern was that if spending slowed too much there was a risk of throwing the economy into a recession.

(If inflation and recessions were a thing back in Homer’s day, he may have thrown Odysseus an extra challenge).

Finally, the inflation story began to turn positive. Inflation in the US, which reached a post-pandemic high of 10%, eased to a point that the Fed began to view inflation as less of a threat and turned their attention toward steering clear of a recession. As a result, they reversed policy and began to lower rates.

The Answer to the Inflation Question

To answer the question we began this post with, inflation—which is generally measured as a year-over-year percentage change—continued to improve and currently stands at a very historically average 2.5%.

Of course, simplifying inflation to a single number can mask areas of concern—like housing costs—which clearly are going to require some more work.

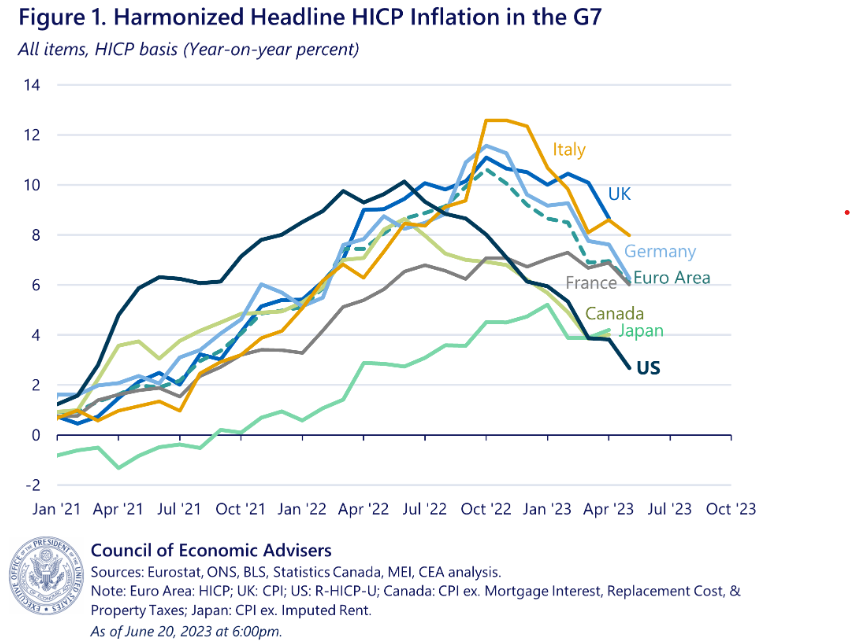

And how has the Fed compared to other Central Banks? So far, pretty good as you can see from the chart below showing inflation in the US is lower than any other G7 country.

And what about recession? Again, so far, so good. The US Gross Domestic Product—a measure of the health of the economy—was up an impressive 5.69% on a year-over-year basis as of September 2024. Meanwhile, wages have grown more than inflation and the US unemployment rate remains below the historical average.

Notably, no Central Bank was able to avoid post-pandemic inflation and the Fed has done a better job than most in getting things back on track.

And, for all we complain about the price of gas, gas prices in the US are about two-thirds the price in Canada and Japan and less than half the price in the other G7 countries—and in Ireland, as we recently experienced, when we hired a car and paid the equivalent of $7.25 per gallon.

Where do We Go from Here?

So, can the Fed declare victory? Hardly, because their job never really ends. It’s a constant challenge to navigate the metaphorical strait between inflation and recession.

At some point, we’ll have another recession in the US, but not all recessions are created equally. Periodic mild recessions are normal and easier to recover from than recessions that we name—like hurricanes—as in the Great Recession of 2008.

And keep in mind that a return of inflation to more normal levels means that the increases in prices are back to historic norms. We’re still stuck with the increase in price levels due to the pandemic.

Now that we’re back to normal, the most likely expectation going forward is that—absent some major change in economic policy—we’ll continue to move forward with average inflation rates.

Can We Go Back?

But can we go back to pre-pandemic price levels?

The short answer is, not likely. The more important question is, do we really want to?

Think, for a moment, about what that would take.

Let’s say a company that was forced to raise prices due to pandemic-related supply shortages was considering lowering prices.

Would they actually do this? Probably not as long as there was demand for their products. Unless everyone back through their supply chain also reduced prices, they’d simply be choosing to make less money—which is not something companies are famous for.

What could force a company to lower prices? Primarily lower demand, i.e., fewer people wanting to buy their products.

And what would lead to this? You got it, a recession.

A recession of sufficient severity would typically lead to layoffs, higher unemployment, and slower wage growth.

In other words, to get back to pre-pandemic levels would require deflation and a high probability of a recession.

So, in reality, the best we can hope for is probably that inflation stays manageable going forward, that wages continue to grow more than inflation, that purchasing power goes up, and that issues like housing costs are effectively addressed.

Economic Heros?

The primary point of this post was to focus on how the Fed uses their ability to set interest rates in an attempt to either speed up or slow down spending.

And while it’s unlikely a modern-day Homer will write an epic poem about the Fed’s recent efforts to navigate the dual threats of inflation and recession—and while there’s clearly still work to be done—it’s probably fair to acknowledge the Fed for a fairly adept handling of a historically difficult situation.

Stuart & Sharon