The Coming Crash?

It's inevitable that we'll experience another stock market Crash—but does it matter?

The stock market is going to Crash.

Fortunately, it doesn’t matter.

Wait! You’re probably thinking, “How can it not matter?”

Let’s qualify that statement and say:

It doesn’t matter with regard to your long-term investment portfolio.

Crashes are Normal

Stock market Crashes are a normal, periodic occurrence in the ongoing life of the stock market.

Speaking of which, do you know when the last stock market Crash occurred and what triggered it?

Think about that for a minute, but first let’s define a Crash. We’ll take a definition from Wikipedia.

A stock market crash is a social phenomenon where external economic events combine with crowd psychology in a positive feedback loop where selling by some market participants drives more market participants to sell.

In other words, a Crash is often a result of panic selling rather than some rational assessment of the valuation of the stock market.

So, how did you do in recalling the last Crash?

It was in 2020 when panic set in as a result of the pandemic. The S&P 500 Index declined nearly 34% over the course of 22 trading sessions.

Pretty scary in the moment.

Recoveries are also Normal

But the moment didn’t last long.

In less than four months, the market had fully recovered from the pandemic losses.

As it turns out, recoveries from Crashes are also normal.

While the recovery from the pandemic Crash was quick by historical standards, you should know that every time we’ve had a market Crash, the market has recovered and gone on to set new record highs—literally 100% of the time.

(This assumes investment in a diversified portfolio, especially a market-cap-weighted index like the S&P 500. If you haven’t done so already, you might want to read our post The S&P 500 (Core Post No 8).

Timing the Market

Now, you might think that since Crashes and Recoveries have happened in the past and will continue to happen in the future that the smart thing to do would be to get out of the market right before a Crash and back in right before the start of a Recovery.

You may not feel you have the background to figure this out but, surely, there must be some “expert” who is proficient in reading the tea leaves. Right?

Unfortunately, the answer is a resounding NO!

Most people—including the “experts”—who try to time the market tend to get out after the market has gone down (or well before it goes down, leaving money on the table) and get back in after it has gone up.

They would have been far better off to just ride it out.

One of the healthiest things you can do for your mental state is to accept that this is true. Otherwise, you’ll just drive yourself crazy.

If you’ve tried in the past to predict the markets, you likely realize how difficult it is. Yet that probably doesn’t stop you from trying again.

Maybe you’ll get it right next time.

Albert Einstein is often quoted as saying:

The definition of insanity is doing the same thing over and over and expecting different results.

We’re not sure Einstein actually said this, but it’s a valid observation nonetheless.

So, quit driving yourself insane by thinking you—or anyone else—should be able to accurately and consistently predict the markets.

A Proper Perspective

Aside from accepting that you can’t do the impossible, what else can you do?

We would suggest learning to put things into a proper perspective.

Let’s start by acknowledging that a Crash certainly does matter if you have stocks in your Short-term Portfolio. But you shouldn’t be doing that, should you?

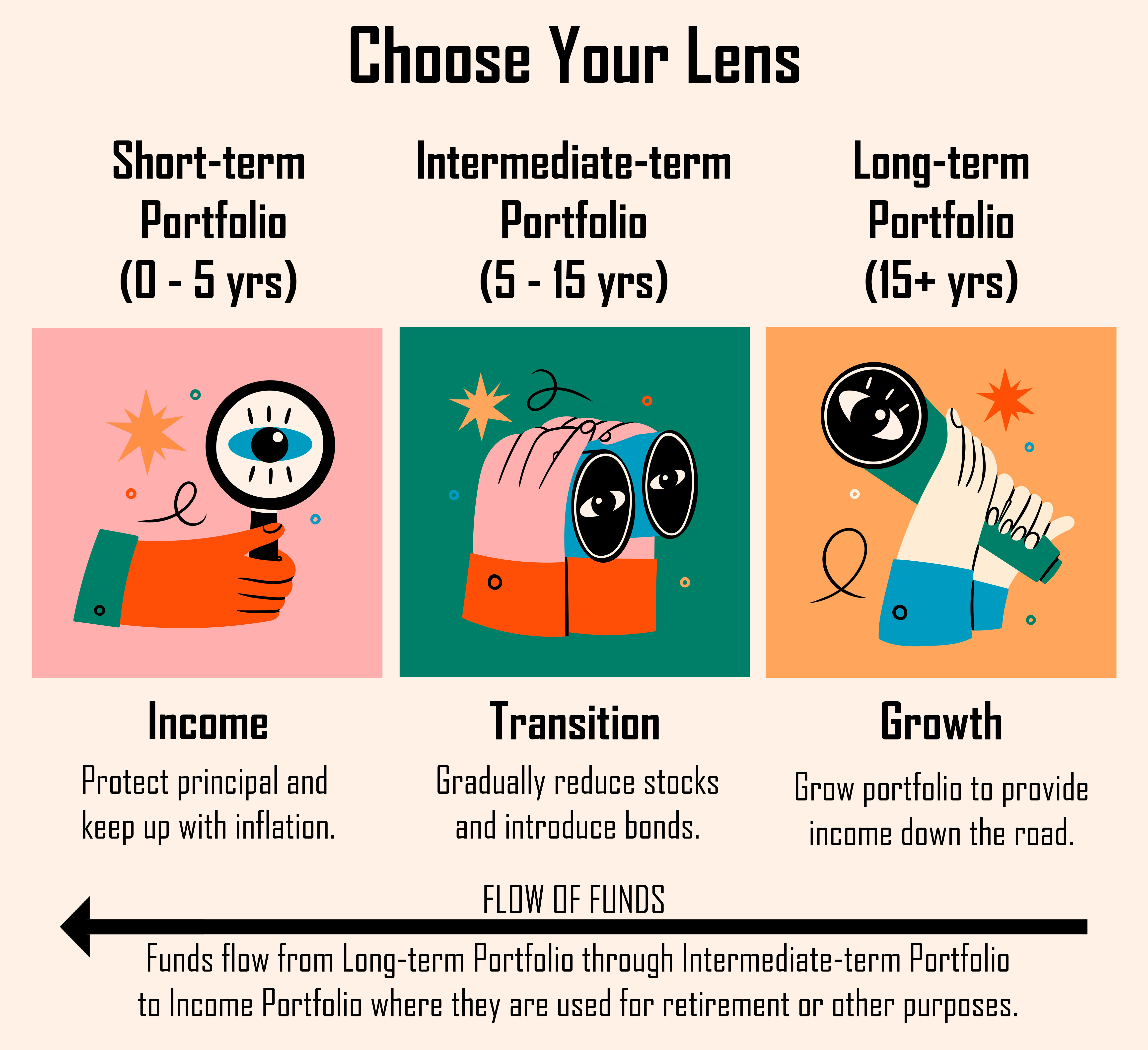

It will help tremendously if you at least mentally divide your investments into a Short-term Portfolio and a Long-term Portfolio and choose the least risky strategy—the one that gives you the best chance of winning—for each.

(And stocks are by far the least risky investment for your Long-term portfolio due to their superior long-term compounding rate.)

Now, it’s very possible that you don’t think of your investments as being divided into a Short-term and Long-term Portfolio (and there’s an Intermediate-term Portfolio between the two also).

Your 401(k) statement doesn’t break it up this way. It’s just one pot of money.

And when it goes down—due to, say, a market Crash—it seems terrifying. Just listening to all the “experts” saying a Crash is right around the corner is scary (even if they’ve been saying this for months, if not years).

The financial industry—and habit, really—tends to force us to look at the stock market through a short-term lens. This makes no sense with regard to your long-term investments.

To explore this more, you might want to check out our post Perspective - Choose Your Lens (Core Post No 3).

An Example

So, what happens if you fail to put things into perspective?

As an example, we’ve heard from a number of people who are quite worried about how the election results might impact the stock market, including some who “got out of stocks” after the last election and are now worried about “getting back in” out of fear that the stock market did far better than they expected and now they feel it is “too high.”

(It’s unlikely they took the time to calculate how much being out of the market cost them.)

But, as we’ve noted before, you should largely ignore who is in the White House when it comes to making long-term investment decisions.

Sure, if things go well, the incumbent will likely claim the credit, and if things go poorly, their opponents will lay on the blame.

But what the political parties do has far less of an impact on the stock market than you might expect.

Consider it this way. Do you think Apple Computer or Nvidia (or any other top company) will find a way to make money under the policies of one party but fail to do so under the policies of the other party?

Of course not.

The best companies in the world will find a way to make money regardless of who is in the White House.

And more to the point, if you invest in the stock market through a market-cap-weighted index (like the S&P 500) it doesn’t really matter which companies figure it out because the ones that are successful will rise to the top of the index.

So, put to rest the notion that the election has much, if any, impact on the stock market.

All you do by worrying about it is to create unnecessary stress, which can be very harmful to your health.

(It’s worth acknowledging that political policy can have an effect on speculative assets like Bitcoin. These cryptocurrencies are, at the moment anyway, more suited to short-term trading/gambling than long-term investing and are for those willing to live with the insane levels of volatility and potential Crashes that are far more severe than we’ll ever see in the stock market.)

A Bubble Ready to Pop?

But what about the notion that the stock market is “too high?” Is the bubble ready to pop?

There are various ways to look at this, but all indicators we’ve seen work best in hindsight and not so well in real-time.

You can look at things like P/E ratios or the state of the Yield Curve, but you may find yourself waiting a long time before these indicators “get it right.”

One of our favorites is a 1965 paper titled, “An inquiry into the Effect of Sunspot Activity on the Stock Market.”

Seriously?

We do like to look at the rolling returns for various time periods for the stock market—not as a timing tool, but rather to get some sense of how the market has been performing.

Since some experts have been suggesting that we’re currently in a 2000-like bubble waiting to burst, it’s interesting to compare where we are now to where we were in March 2000.

5-Year Return

Nov 2024: 16.37% (77th percentile)

Mar 2000: 26.76% (99th percentile)

Comment: stocks have performed much better than average over the last 5 years (77th percentile) but nowhere near the historically record high levels of March 2000 (99th percentile).

10-Year Return

Nov 2024: 13.64% (64th percentile)

Mar 2000: 18.84% (98th percentile)

Comment: stocks have performed somewhat better than average over the last 10 years (64th percentile) but again, nowhere near the historically record high levels of March 2000 (98th percentile).

20-Year Return

Nov 2024: 10.82% (50th percentile)

Mar 2000: 18.27% (100th percentile)

Comment: stocks have performed at an average level over the last 20 years (50th percentile) versus historically record high levels of March 2000 (100th percentile).

So, basically, stocks have done rather well in recent years, but if we step back a little, we see they have been exactly average over the past 20 years.

(One interpretation of this is that it was necessary for recent returns to be above average in order to bring the longer-term 20-year return back up to average.)

In contrast, in March of 2000 nearly all return periods were at or near all-time record highs.

It’s hard to make the case the stock market of 2024 is the same as the stock market of early 2000.

In other words, there’s no reason to panic.

Of course, if you separate your Short-term and Long-term investments, there’s never a reason to panic. Don’t put stocks in your Short-term portfolio and you don’t have to worry about the next Crash.

In Summary

Yes, the stock market will Crash again. And then it will Recover.

Trying to time the market will drive you crazy and likely cost you a lot of money.

Once you grasp this, you’ll be a step closer to achieving what we consider to be the ultimate payoff of these posts: More Money; Less Stress.

Stuart & Sharon