The S&P 500 (Core Post No 8)

How the world's second most famous stock index has an unfair advantage that you can take advantage of.

The S&P 500 cheats.

Or at least it seems that way if you’re an investor or fund manager trying to “beat the index.”

On the other hand, if you’re an investor trying to achieve your financial goals by securing a sufficiently high long-term compounding rate, this is a good thing.

Before we explain why, let’s take a quick look at the history of the world’s second most famous stock market index.

A Brief History of the S&P 500

In 1860, Henry Poor published History of Railroads and Canals in the United States, containing financial information about U.S. railroad companies, and began publishing an annual edition of Poor’s Railroad Manual (which had cool pictures of trains on the cover).

As we noted in our post on The Dow (Core Post No 7), railroads were the thing during the second half of the 1800s and railroad securities dominated the investment world.

In 1923 Standard Statistics Company began publishing a daily stock market index consisting of 90 stocks. The index was expanded to 500 stocks in 1954.

Standard Statistics Company merged with Poor's Publishing in 1941 to form Standard & Poor's.

From that point on, the index has been known as the Standard & Poor’s 500, or the S&P 500 for short.

The company’s indices are now under the umbrella of S&P Dow Jones Indices.

A Market-cap-weighted Index

You may recall from our prior post that the world’s most famous stock index—the Dow Jones Industrial Average—is a price-weighted index. The size of the company doesn’t matter, just the price.

Unlike the Dow, the S&P 500 is a market-cap-weighted index. (The “market cap” of a stock is simply the stock price times the number of shares outstanding.)

In the S&P 500, size matters. And it’s a big deal.

Riding the Winners

What this means is that the S&P 500 basically “rides the winners.”

Pause for a moment to ask yourself how you make money when you invest in stocks.

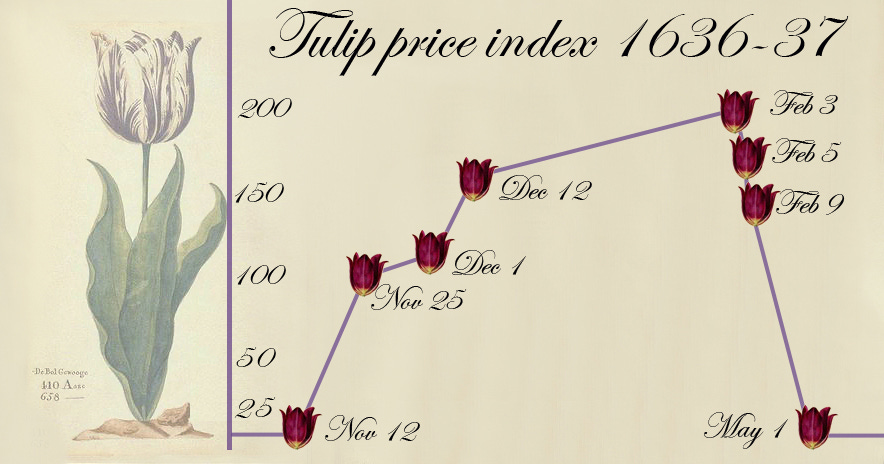

How does this differ from an investment in, say, Bitcoin or tulip bulbs? (And yes, tulip bulbs were a major investment in Denmark in the 1600s.)

Let’s start with stocks.

Companies are in business to make money. If you’re a shareholder, you participate in the company’s success or failure to turn a profit.

Companies that prove themselves and do well over time grow and become increasingly more valuable.

For example, since its founding in 1976, Apple has proven itself and has consistently held a position among the top 3 largest publicly traded companies in the world.

In contrast, Bitcoin and tulip bulbs do not earn money in the same way companies do. Because of fluctuations in value, it is (or was, in the case of tulip bulbs) possible to make money as long as someone was willing to pay a higher price (sometimes for irrational reasons).

These speculative assets are also susceptible to crashes (the tulip bulb market never recovered) and are more suitable for short-term trading or gambling than long-term investing.

Because the S&P 500 is market-cap-weighted, successful companies gravitate toward the top of the index over time while companies that falter or fail become an increasingly smaller drag on the performance of the index.

An Unfair Advantage

This gives the S&P 500 an unfair advantage relative to anyone trying to construct a portfolio attempting to beat the index.

Consider the following analogy.

Imagine that you’re an NFL analyst and, prior to the start of the season, you are tasked with the job of picking the 14 teams that will end up with the highest combined win total. You’re trying to beat a pre-defined index.

But here’s the catch. The index in question will automatically own the 14 playoff teams.

Beating this index would be a tall task.

And so it is with trying to beat the S&P 500.

Because of the way it’s constructed, the top 10 stocks in the S&P 500 (as of the date of this post) make up 36% of the index and the top 25 stocks make up 49%.

The top two stocks alone have a higher combined weight than the bottom 300 stocks in the index.

Some people believe that having a high percentage of an index concentrated in a few stocks is a disadvantage. It isn’t. It’s a major advantage, borne out by the data.

S&P Global publishes data on the percentage of stock funds that beat the S&P 500 over various time periods. The latest results are as follows:

1 Yr: 43% of fund managers beat the S&P 500

3 Yrs: 14% beat the index

5 Yrs: 23% beat the index

10 Yrs: 15% beat the index

What these numbers don’t show is that the funds that were able to beat the index in one period weren’t able to sustain their outperformance in subsequent periods.

Ultimately, the goal of investing in the stock market is to capture the historical long-term compounding rate for stocks. It’s not about trying to beat the index, but rather going along for the ride and capturing the value of the index.

If you try to build a portfolio to beat the index, you’re depending on your ability to identify and buy the best stocks. It’s possible, but not likely.

The Story of Nvidia

Before we leave, let’s talk about Nvidia.

Nvidia was founded in 1993 and, by the late 90s, was one of 70 start-up companies betting that graphic acceleration for video games was going to be a big deal.

It was hardly smooth sailing for Nvidia and, after laying off half of their workforce in 1997, they were down to 40 employees and facing legitimate questions as to whether they could continue. The unofficial company motto became, “Our company is thirty days from going out of business.”

Things turned around in 1998 and the company went public in 1999. An early breakthrough occurred when Nvidia won the contract to produce the graphics hardware for Microsoft's Xbox game console.

More recently, Nvidia GPUs were in high demand for cryptocurrency data mining, meaning that you could benefit from the crypto craze without the need to invest directly in Bitcoin and other highly volatile cryptocurrencies.

Of the original 70 start-ups trying to win the graphic acceleration race, only two survived (the other was ATI Technologies, acquired by ADM in 2006, and now the 30th largest publicly traded company).

And only the survivors that grow to a sufficient size make it into the S&P 500. Nvidia was added to the index in November, 2001 (replacing Enron).

The moral of the story is that as an investor in the S&P 500, you didn’t need to identify Nvidia as a future winner (you may not even have heard of Nvidia in 2001).

But if you owned the index—which you can easily do through an index fund or exchange-traded fund—you were automatically invested in Nvidia.

And you never would have owned the other 68 start-ups that failed.

Ironically, Nvidia is being added to the Dow as of the date of today’s post—November 8, 2024—replacing Intel (Sherwin-Williams is also being added, replacing Dow Inc.).

If you owned the S&P 500, you would have benefited from the rise in Nvidia from a company that was 30 days away from going out of business to a company that just overtook Apple as the largest publicly traded company in the world.

If you owned the Dow, you wouldn’t have gotten into Nvidia until 2024—and would have missed out on an annualized return of over 29% since Nvidia joined the S&P 500 twenty-three years earlier.

The Nvidia story is the epitome of “riding the winners.”

The Takeaway

Our primary goal with this post was to familiarize you with an index that we believe is an excellent choice for anyone investing in the stock market.

Will it always be the best stock market fund? Of course not. But trying to find a fund that can consistently beat it is a challenge. And, if all you care about is making money, it’s essentially unnecessary.

The ability to capture the value of investing in the stock market without a lot of effort is the hallmark of the more money; less stress premise we’ve been promoting throughout these posts.

Stuart & Sharon