Compounding: the 3 - 5 - 10 Rule

Use these numbers to make smart decisions.

Most of what we’ve written in these posts is designed to help you make smart financial decisions automatically. It’s what we call Financial Mastery and helps fulfill the promise of these posts:

More money; Less stress

To help with this, we’ll sometimes create simple rules.

The rule we’re introducing in this post is the 3 - 5 - 10 Rule, and it relates to Compounding.

Compounding—as you’ll recall—is the secret to investing.

It seems too good to be true. But it isn’t!

If you need a refresher, look at our post, The Most Important Number to Know About Your Portfolio.

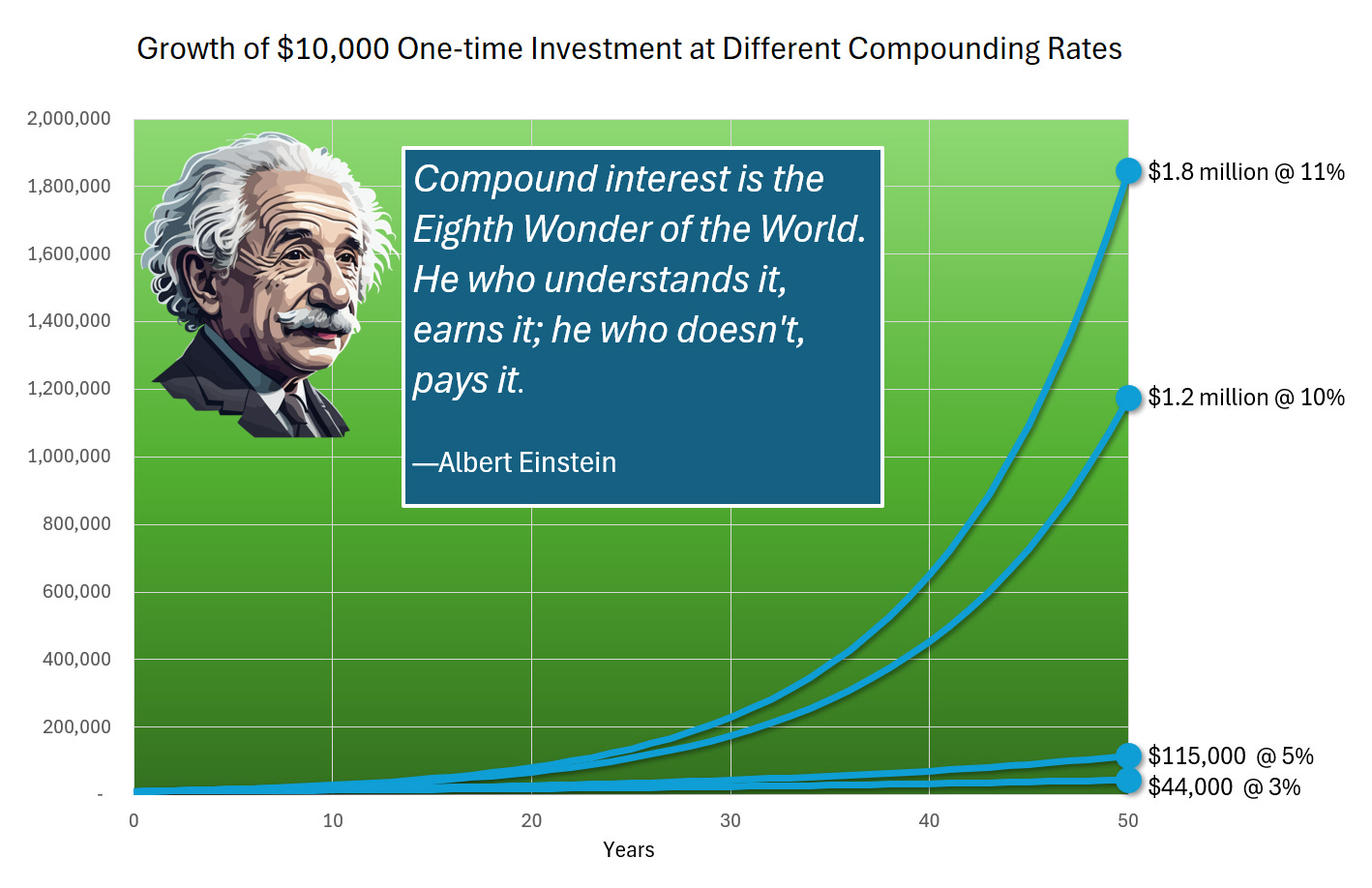

The critical part of that post was the difference in how much you can make depending on the Compounding Rate.

We compared the growth of a one-time investment over 40-year and 50-year time periods using 3%, 5%, and 10% Compounding Rates.

What we didn’t cover was which investments can achieve these rates, and we didn’t cover the fact that your actual experience could be higher or lower than these long-term averages.

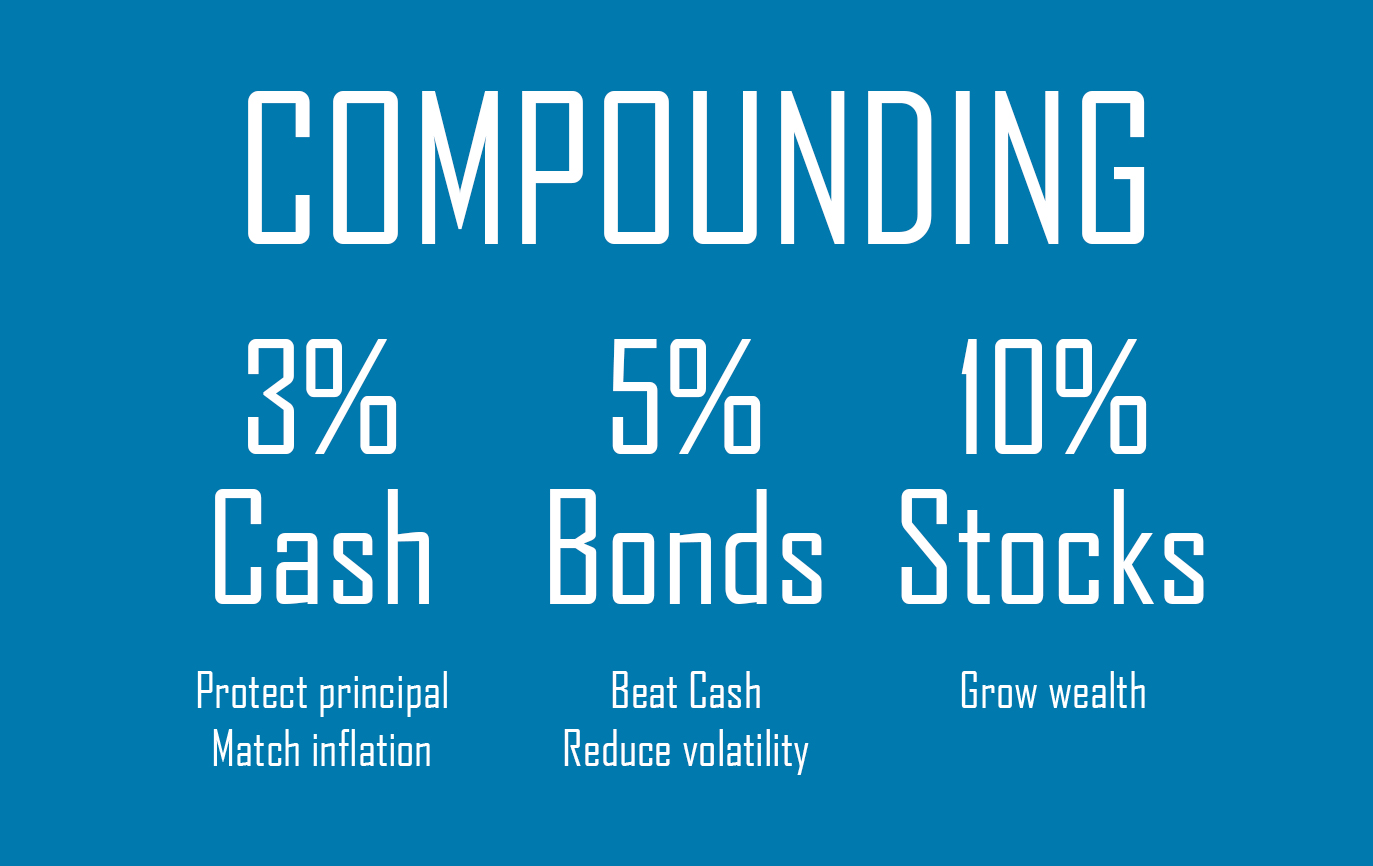

So, let’s look at the major asset classes (Stocks, Bonds, and Cash) and see what you can expect.

Compounding at 3% with Cash (Short-term Investments)

Since 1926, the long-term compounding rate on Cash (Short-term Investments) has been just over 3% (based on 3-month Constant Maturity US Treasuries).

Over that same time period, the long-term compounding rate on Inflation (CPI-U) has been just under 3%.

Short-term investments are great at protecting your principal while keeping up with inflation.

They are an ideal fit for your Short-term Portfolio (3 to 5 years), but won’t help you grow long-term wealth.

They are the least risky investment in the short run, but the most risky investment in the long run.

Compounding at 5% with Bonds

The long-term compounding rate for bonds (based on 10-year Constant Maturity US Treasuries) is between 4% and 5%. If you invest in a bond index fund that includes bonds other than Treasuries, we’re going to assume you can do a bit better, so we’re rounding this up to 5%.

In the long term, Bonds should be expected to beat Cash and Inflation, but are nowhere near as powerful as Stocks in terms of growing wealth.

Bonds are best suited to your Intermediate-term Portfolio, primarily as a way to reduce intermediate-term portfolio volatility.

Compounding at 10% with Stocks

When it comes to growing long-term wealth, Stocks are where it’s at.

The long-term compounding rate on Stocks (we’re using the S&P 500) is a bit over 10%.

As we discovered in our last post, the difference between compounding at 10% versus 5% is enormous—in fact, it’s life-changing.

And 10% is probably a bit conservative. If we exclude the 1930s—the Wild West for stocks with very few guardrails—the long-term compounding rate is a bit over 11%.

How much could 1% matter? Scroll back up and look at the chart!

A Rule to Help Put Long-term Decisions in Perspective

Keep in mind that we’re using round numbers here as an easy-to-remember Rule to help with Decisions.

The general gist is this:

Short-term investments (Cash) are a great way to protect your principal while keeping up with inflation.

Bonds should earn more than Cash over time and can help reduce volatility in your Intermediate-term Portfolio, but are no match for Stocks in terms of long-term earnings potential.

Stocks are the path to long-term wealth and financial security, but are not suitable for your Short-term Portfolio due to short-term volatility.

Compounding 3 - 5 - 10

Ultimately, Compounding 3 - 5 - 10 is just a simple Rule to help you put the roles of the major asset classes in perspective.

Best regards,

Stuart & Sharon